Smart Lock Market Share Forecast 2030

June 22, 2026 · 11 min read

Smart Lock Market Share Forecast 2030

By 2030, I’d plan for a smart lock market of about _$7 billion to $10 billion_ globally, with share moving toward brands that pair lock hardware with strong software, remote access, and booking-friendly integrations.

If you just want the short version, here it is:

- North America still leads smart lock sales today, at about 37% to 41% of revenue.

- Asia-Pacific is growing fastest, helped by new housing and mobile-first access.

- Bluetooth leads now, but Wi-Fi, [Thread](https://threadgroup.org/), and [Matter](https://en.wikipedia.org/wiki/Matter_(standard)) are getting more attention for remote control and cross-device support.

- [ASSA ABLOY](https://www.assaabloy.com/group/en), [Allegion](https://www.allegion.com/), and [dormakaba](https://www.dormakabagroup.com/en) start from the strongest position.

- By 2030, I’d expect share gains to come less from lock design and more from API access, app quality, remote credential control, and software fit.

- For rental fleets, the big question is simple: _can the lock plug into booking, ID, and pickup workflows without staff stepping in?_

That’s the core takeaway. The market is growing, but the bigger shift is _what buyers are paying for_. It’s no longer just a deadbolt with an app. It’s part of an access system. This shift is a key part of how companies automate rental business operations to reduce overhead.

My read: if you run rentals, storage, trailers, bikes, or equipment handoffs, you should judge smart locks in this order:

- Remote code management

- Offline PIN fallback

- Booking and API support

- Battery and connectivity fit

- Brand and hardware style

Digital Door Lock System Market, Global Outlook and Forecast 2023-2030

sbb-itb-eb44693

Quick comparison

| Area | What I’d expect by 2030 | | --- | --- | | Market size | $7 billion to $10 billion planning range | | Current leaders | ASSA ABLOY, Allegion, dormakaba | | Top buying factor shift | From hardware specs to software ecosystem fit | | Main connectivity trend | Bluetooth stays large; Wi-Fi and Matter/Thread gain ground | | Fast-growth use cases | Hospitality, shared access, [trailer rentals](https://www.lockii.app/post/igloohome-powered-trailer-rentals-automate-business), self-serve pickup | | Best-placed vendors | Brands with remote access tools, platform links, and fleet-friendly control |

If I had to sum up the article in one line, it would be this: the brands most likely to hold or gain share by 2030 are the ones that make access easier to manage at scale, not just easier to install.

Smart Lock Market Outlook to 2030

Global market size, CAGR, and differences across published forecasts

Published smart lock forecasts are all over the map. The main reason is simple: research firms don’t all define the market the same way. Most put the 2024–2025 baseline at $2.95 billion to $3.23 billion, while broader market definitions push it up to $4.83 billion [7][8]. And because the forecast periods don’t line up neatly, the 2030 outlook works best as a planning range, not a single hard number.

The forecasts that matter most for a 2030 view are below:

| Research Firm | 2024–2025 Baseline | Forecast Value | Forecast Year | CAGR | | --- | --- | --- | --- | --- | | Mordor Intelligence | $3.23 billion | $7.52 billion | 2031 | 15.11% [2] | | Future Market Insights | $3.10 billion | $9.40 billion | 2036 | 11.6% [4] | | Renub Research | $3.12 billion | $11.77 billion | 2033 | 18.05% [9] |

Put those side by side, and a practical 2030 planning range is $7 billion to $10 billion [2][4][9]. That spread isn’t just a research quirk. It starts to show up pretty fast once you look at regional demand.

Regional growth patterns in North America, Europe, and Asia-Pacific

North America has the largest share of the global smart lock market today, making up about 37.05% to 40.7% of total revenue in 2025 [2][6]. That lead comes from early adoption, a strong DIY retrofit market, and steady demand through builders and housing channels. In a more mature market like this, companies with strong app ecosystems and hardware that works well in retrofits have a better shot at holding or growing share.

Asia-Pacific is growing the fastest, with projected CAGRs of 15.42% to 24% through the mid-2030s [2][6]. A big part of that comes from large-scale housing construction in China and India, where mobile-first access is often built in from the start instead of added later.

That split matters. Mature markets lean harder on retrofit ease and software tie-ins, while fast-growth markets can move more directly toward mobile-first access at scale.

Segment trends by application, hardware format, and connectivity

Among applications, hospitality is growing the fastest, with a projected 17.05% CAGR [10]. Hotels and short-term rental operators are moving away from RFID card systems and toward mobile check-in plus automated guest access. That shift changes what buyers care about. It’s less about the lock alone and more about how smoothly the system works day to day.

On hardware, deadbolts still lead, with 45.12% to 49.5% of total revenue [2][6]. They’re the current standard in many residential installs. At the same time, lever handle locks are growing the fastest, at 15.18% to 16.21% CAGR [2][10], helped in part by ADA compliance needs in commercial settings.

Connectivity tells a similar story. Bluetooth leads today, with a 49.0% to 61.68% share [4][2]. It’s common, familiar, and easy to deploy. But Wi-Fi is growing the fastest, with a projected 16.02% CAGR [10], because it allows real-time remote management.

For rental and hospitality operators, that point is hard to ignore. Wi-Fi and Zigbee/Thread Matter-compatible locks are becoming more important because they support remote control and better interoperability [2][8]. By 2030, lock share is likely to depend less on the physical format and more on software fit, remote management, and how well the lock works inside a broader device ecosystem.

For operators in rentals and hospitality, connectivity choice is starting to shape which manufacturers win share by 2030.

Competitive Landscape and Manufacturer Share Shifts

2023 Positioning

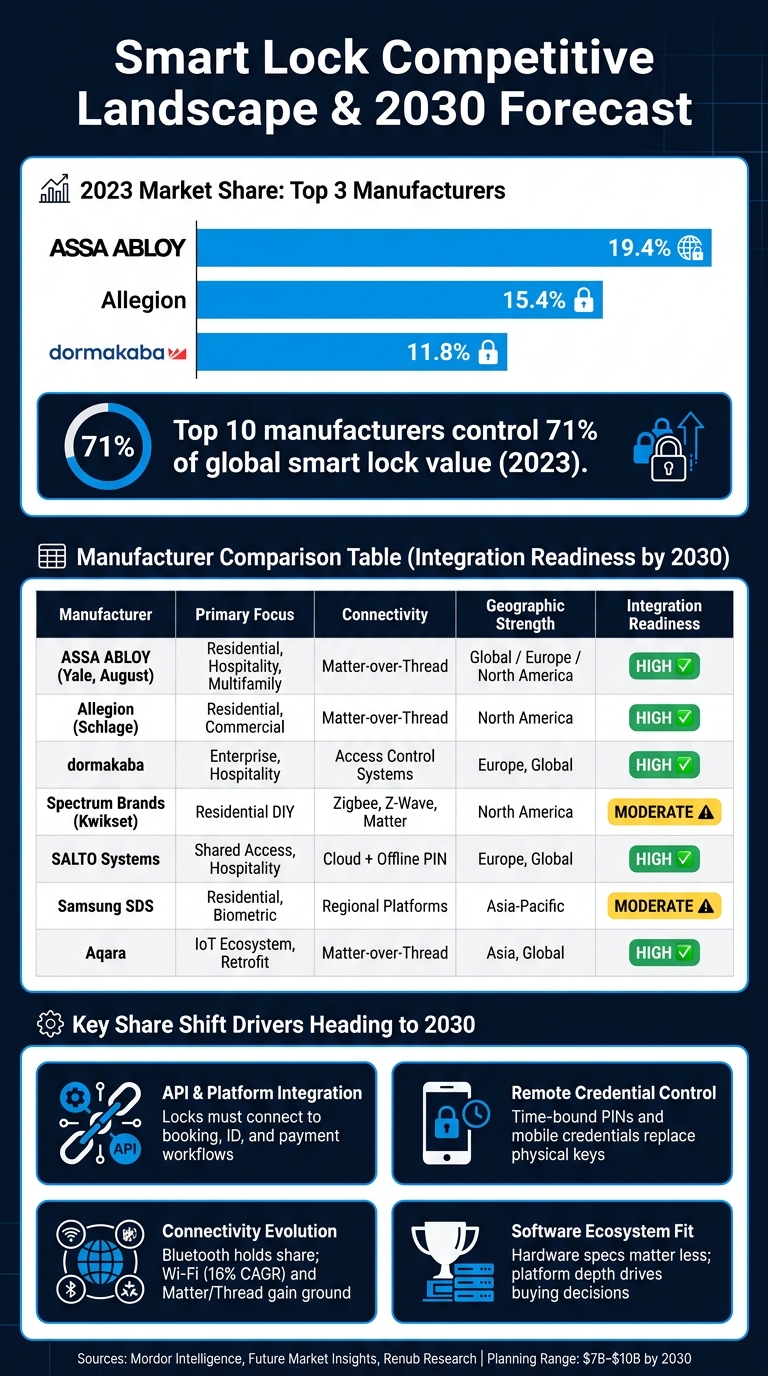

This market is concentrated. In 2023, the top ten manufacturers held 71% of total global market value [10]. The three biggest players were Assa Abloy at 19.4%, Allegion at 15.4%, and dormakaba at 11.8% [10].

Their edge isn't just the lock itself. It comes from the system around it.

Assa Abloy stands out in consumer and rental-access links. Allegion has strength in biometric-enabled access. dormakaba is well placed in enterprise and hospitality.

That matters because the path to 2030 looks less like a hardware race and more like a platform race. Brand name still helps, sure, but integration depth is starting to matter more.

How Market Share May Shift by 2030

By 2030, manufacturers that control both software security and dependable hardware are more likely to protect share than brands focused mostly on hardware [4]. If a company mainly competes on specs, the job gets tougher. Buyers are looking at more than form factor and price now. They also care about whether a lock fits the rest of their setup. This integration is a core driver behind the benefits of 24/7 contactless rentals in commercial and residential sectors.

[Aqara](https://www.aqara.com/us/) could pick up incremental share in Asia-Pacific as Matter-over-Thread adoption grows.

The comparison below shows which manufacturers look best placed to hold or gain share.

Manufacturer Comparison Table: Portfolios and Integration Readiness

The comparison below highlights the capabilities most likely to influence share by 2030.

| Manufacturer | Key Brands | Primary Focus | Connectivity | Geographic Strength | Integration Readiness | | --- | --- | --- | --- | --- | --- | | Assa Abloy | Yale, August, Mul-T-Lock | Residential, Hospitality, Multifamily | Matter-over-Thread | Global; strong in Europe and North America | High - rental-platform integration, Matter, Aliro | | Allegion | Schlage | Residential, Commercial, Multifamily | Matter-over-Thread | North America | High - Biometrics, Apple Home Key | | dormakaba | dormakaba | Enterprise, Hospitality, Commercial | Access control systems | Europe, Global | High - Enterprise access control | | [Spectrum Brands](https://spectrumbrands.com/) | Kwikset, Weiser | Residential (DIY & Builder) | Zigbee, Z-Wave, Matter | North America | Moderate - DIY retrofit focus | | [SALTO Systems](https://saltosystems.com/en-us/) | SALTO | Shared access, Commercial, Hospitality | Cloud-based management, offline PIN/RFID | Europe, Global | High - Cloud management, offline PIN | | [Samsung SDS](https://www.samsungsds.com/us/index.html) | Samsung | Residential, biometric-heavy | Regional platforms | Asia-Pacific | Moderate - Strong regionally | | Aqara | Aqara | IoT ecosystem, retrofit | Matter-over-Thread, Apple Home Key | Asia, Global | High - Matter, AI features |

Segment-Level Forecasts for Rental, Hospitality, and Shared Access

Bluetooth, Wi-Fi, keypad, and offline PIN share trends

Demand by segment now makes it clear where these connectivity changes matter most. In rentals and short-term stays, Bluetooth still leads because it works without a router or steady internet. It held a 61.68% share of the smart lock connectivity market in 2025 [2], and forecasts place it at 49% to 52% by 2030 [4][5].

Wi-Fi is picking up in cloud-managed systems that focus on direct remote control without a separate hub. That segment is set to grow at a 16.02% CAGR from 2023 to 2028 [10]. The catch is simple: Wi-Fi usually puts more strain on battery life.

Keypad and offline PIN access still matter a lot. PIN code authentication made up 42.3% of the market in 2023 [10], and it stays central in places where internet service is shaky, especially trailer yards and equipment depots. In those settings, offline access isn't a nice extra. It's the thing that keeps operations moving.

Matter-over-Thread is the main option to watch here, mainly because it aims to stretch battery life and improve interoperability.

These access methods matter for a simple reason: not every rental setup needs the same level of automation.

Demand drivers in commercial, hospitality, mobility, and self-hire

Hospitality is moving toward time-bound PINs and mobile credentials to cut out physical key handoffs. Short-term rental platforms are also linking up with lock brands to automate reservation-timed door codes. Mobility and self-hire are heading in the same direction.

For rental operators, the issue is pretty plain. How do you hand off a rental when nobody on staff is there? The market's answer is automated pickup: a booking triggers a time-limited lock code, and the customer gets access without a manual handoff.

Lockii fits that shift by linking digital locks to booking workflows for 24/7 self-hire pickup without staff.

Segment share and growth comparison table by use case

The table below breaks out the segments that matter most for contactless rental operators.

| Segment | 2023 Est. Share | 2030 Proj. Share | CAGR | Common Access Methods | | --- | --- | --- | --- | --- | | Residential | 58.5% [10] | Largest segment [4] | 11.6%–14.4% [10][4] | App-based, PIN, biometric | | Hospitality | ~15%–18% [3] | Expanding [1] | 23.8% [1] | Time-bound PIN, Bluetooth, mobile key | | Commercial / Enterprise | ~10%–12% [3] | Steady growth [2] | 15.18% (lever handles) [2] | RFID/NFC, keypad, audit trails | | Mobility & Rental | Emerging | Growing [4] | High (Niche) [4] | Offline PIN, Bluetooth, remote API |

Residential still leads on volume. But the fastest growth is showing up in hospitality and mobility. By 2030, the practical test is whether a lock system can handle booking-triggered access, audit trails, and remote control.

What the 2030 Forecast Means for Contactless Rental Operators

Why integration-ready lock ecosystems matter) more than hardware alone

By 2030, market share is likely to depend less on the lock itself and more on how well the software connects with the rest of the rental stack. Buyers already care more about phone and platform compatibility than finish or looks.

For multi-site U.S. rental operators, the issue is pretty simple: they need locks that can handle remote code updates and connect with booking, payment, and ID systems. If a lock can't do that, staff end up doing manual work at every handoff. Across a fleet, that friction adds up fast.

That shifts the first buying test. For rental operators, workflow fit matters more than device specs.

How Lockii fits the shift toward automated self-hire

That workflow gap is exactly why rental automation matters more than AI for most operators. Lockii is built for rental operators managing trailers, equipment, bikes, or vehicles across multiple sites.

Here's how it works:

- A booking triggers a time-limited lock code

- Identity is verified before pickup

- The customer gets SMS and email instructions without staff involvement

This setup supports 24/7 unattended pickup across multi-location fleets. That lines up directly with the market move toward access systems built for software connection, remote control, and less hands-on work.

Manufacturers with stronger APIs and remote credential management are more likely to gain share by 2030. The same idea applies to operators: those who build around connected workflows are in a better spot to scale without adding headcount.

The most likely market outcomes by 2030

For operators, the signal is clear. By 2030, the winners are likely to be the vendors and rental businesses built around remote management, offline fallback, and strong integrations.

The operators with the best odds of growth won't treat lock hardware as a standalone device. They'll treat it as one part of a larger automated workflow, which helps them grow without matching every gain in revenue with more labor or overhead.