Michigan Trailer Rental Insurance: What to Know

June 15, 2026 · 9 min read

Michigan Trailer Rental Insurance: What to Know

If I rent out trailers in Michigan, I can’t assume the renter’s auto policy will cover the loss. A claim can fail in _three separate places_: liability, No-Fault, or damage to the trailer itself. And for many fleets, physical damage coverage often costs about $200 to $600 per trailer per year, which is small next to a six-figure claim.

Here’s the short version:

- Trailer type matters in Michigan. Some trailers may need their own No-Fault coverage, especially depending on axle and wheel setup.

- Liability coverage is not damage coverage. A renter’s tow vehicle policy may cover injury or damage to others while towing, but it often won’t pay for the rented trailer if it is damaged, stolen, or vandalized.

- General Liability often won’t fix inventory damage. The common issue is property in the renter’s possession.

- Inland Marine coverage is often the policy that fills the trailer-damage gap, including theft or damage while the trailer is unhitched, if the form allows it.

- A COI alone is not enough. I need to check expiration date, limits, covered use, and whether the policy fits the trailer being rented.

- The rental contract matters. It should say who pays deductibles, what uses are banned, how trailer damage is handled, and whether business use needs written approval.

- The [pickup process needs to be the same every time](https://www.lockii.app/post/trailer-rental-safety-checklist-generator) to ensure safety and compliance. ID check, tow vehicle details, insurance review, signed terms, and timestamped photos before and after the rental.

Bottom line: if I run a Michigan trailer rental business, I need to line up the right policy for each trailer type, clear renter terms, and the same check-in process at every location.

| Topic | What I need to check | | --- | --- | | No-Fault | Whether that trailer type needs its own Michigan coverage | | Liability | Whether the renter’s towing policy covers the trip and use | | Trailer damage | Whether my policy covers theft, vandalism, collision, and unhitched loss | | Paperwork | COI details, signed rental terms, photos, timestamps |

This article explains where claims usually break down and what I should set up before the first rental leaves the lot.

How to Insure a Work Trailer (Commercial Auto vs Inland Marine)

Michigan trailer insurance basics

Michigan treats some trailers as motor vehicles under Michigan No-Fault rules. That means trailer type and wheel count can change whether a unit needs its own coverage. Before you rent anything out, document how each trailer is classified. Each trailer type needs its own coverage call.

When a trailer needs its own Michigan No-Fault coverage

A standard single-axle utility trailer with two wheels may not need its own No-Fault policy. But a tandem-axle enclosed trailer or another multi-wheel equipment hauler may need separate No-Fault coverage. Get that classification confirmed in writing for every trailer type.

Liability coverage does not equal damage coverage for the rented trailer

Even if liability is handled, damage to the trailer is a separate risk. The towing vehicle's liability policy covers third-party bodily injury and property damage claims. It does not pay to repair or replace the rented trailer itself if it's damaged, stolen, or vandalized.

General Liability usually excludes property in a renter's possession, so it often won't pay for damage to a rented trailer. As Ryan Keen, HQRent, says:

"The care/custody/control exclusion in GL means damage to rental inventory isn't covered by the policy most operators think of as their primary protection." [3]

Physical damage to the trailer is usually covered by an Inland Marine policy, which often runs $200–$600 per year per trailer [1][2]. When you buy that coverage, push for stated value or replacement cost, not ACV. Why does that matter? Because for rental fleets, one loss can turn into a full replacement-cost hit. ACV can leave a big gap that comes out of your pocket [3].

Coverage rules are only the first layer. The next place things go wrong is proof, contracts, and branch procedures that aren't handled the same way every time. Many operators automate trailer hire to ensure these checks and contracts are completed consistently without manual oversight.

Common insurance compliance gaps for Michigan trailer rental businesses

Once the coverage rules are clear, the next place things break down is day-to-day verification.

Assuming the customer's auto policy covers every trailer and every use case

This is where many rental businesses get burned. The key issue isn't whether the customer _has_ insurance. It's whether that policy covers the exact trailer type and the way it's being used when a claim happens. Staff should check whether the renter's policy excludes the trailer type in question or excludes commercial rental use [1]. If that check doesn't happen before pickup, the business can end up with an uninsured loss. Book the wrong trailer under the wrong policy, and the claim may not be paid.

"Personal auto policies are not designed for commercial rental activity - they're designed for personal use. The exclusion is in the policy language and it's enforced at claim time, not at policy purchase time." - Pablo Fernandez, Big Rentals [1]

There's also a common gap with unhitched trailers. Once a trailer is detached at a job site or a residence, a standard business auto policy will usually stop covering it. That's a physical damage problem, not a liability problem. If the trailer is stolen or vandalized while sitting unhitched, only an Inland Marine policy will respond [3].

Missing proof of insurance, weak contracts, and inconsistent branch checks

A COI is not the same as verification. If the COI is expired, shows limits that are too low, or doesn't match the trailer type being rented, it's just paper [3].

"A certificate of insurance (COI) is a document from the renter's insurer confirming active coverage. Accepting a COI at face value without reviewing it is a paperwork exercise, not a risk management exercise." - Ryan Keen, HQRent [3]

The contract matters just as much. Weak rental agreements often lead straight to claims fights. If the agreement doesn't spell out who pays the deductible, which uses are banned, and how damage to the trailer itself is handled, those issues get debated after the loss instead of settled before it.

Branch-to-branch inconsistency makes the problem worse. If one location checks insurance one way and another does it differently, the whole operation is exposed. In a multi-location business, one weak branch can hurt the claims position for everyone.

That’s why rental businesses need the same coverage terms, the same review steps, and the same branch procedures before the first trailer leaves the lot.

How to structure coverage and rental terms for Michigan compliance

Once you’ve identified the gaps, the next step is simple: close them in the policy and in the [rental contract and service agreement](https://www.lockii.app/licenses).

Build a baseline fleet coverage plan by trailer type

A good starting point is three layers of coverage:

- Commercial Inland Marine for the trailer itself

- CGL for third-party claims

- Business Auto for company pickups and deliveries

Make sure the Inland Marine policy covers trailers while they’re in the customer’s possession and while unhitched. That point matters more than it may seem. Some policies leave those situations out, so get written confirmation from your broker [1].

For valuation, use stated value or replacement cost instead of ACV.

Write clear renter terms for liability, damage, and commercial use

Your renter terms need to say, in plain English, who handles what.

Require proof that the tow vehicle has active liability coverage. Make the renter responsible for trailer damage while the trailer is in their possession. And if certain uses are off-limits, or if business use needs approval, put that in writing. For commercial use, require written approval before the rental starts.

Be just as clear about deductibles. If you offer a damage waiver, spell out exactly what it covers, what it does not cover, and where the renter still has exposure. That includes cases like theft from an unsecured trailer if that does not qualify under the waiver. Also state that a damage waiver does not replace third-party liability coverage.

Those terms only hold up if staff check them the same way at every pickup.

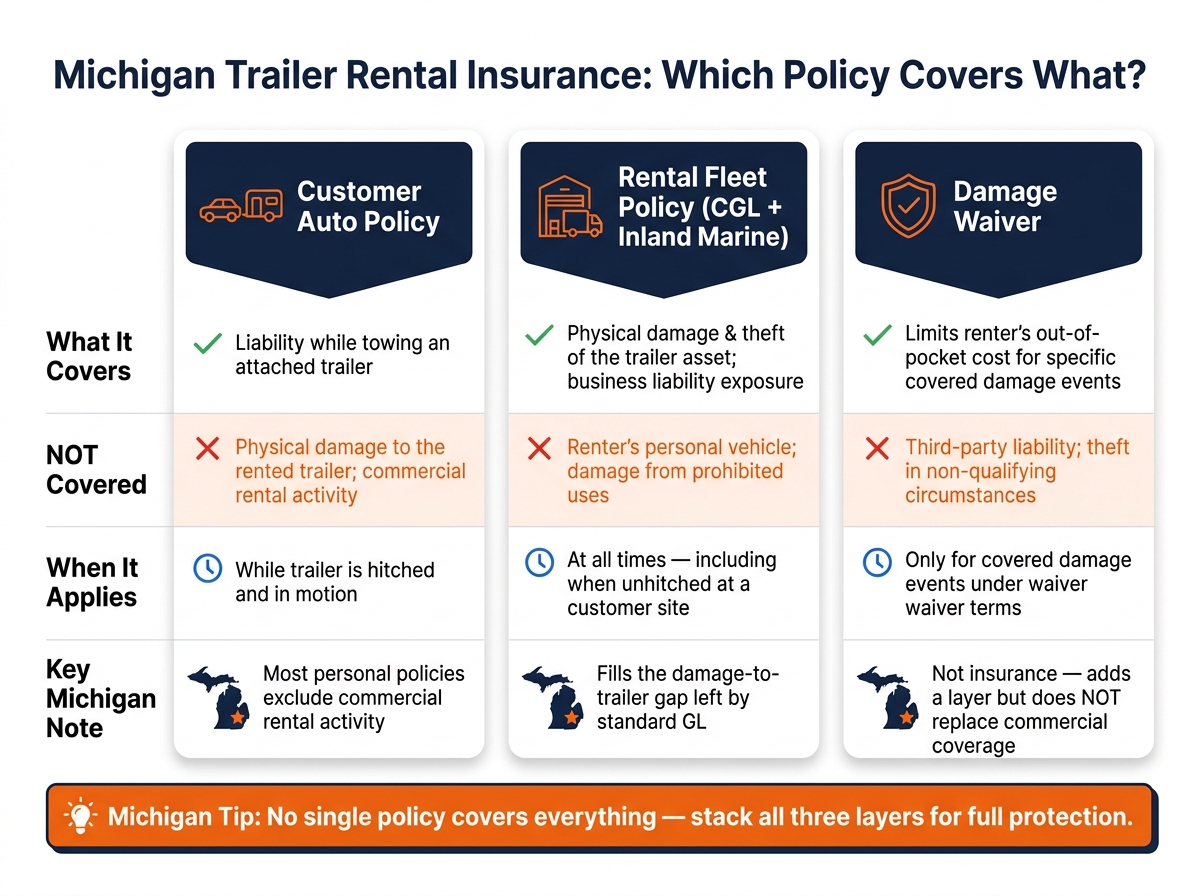

Comparison table: customer auto policy vs. rental fleet policy vs. damage waiver

| | Customer Auto Policy | Rental Fleet Policy (CGL + Inland Marine) | Damage Waiver | | --- | --- | --- | --- | | What it covers | Liability while towing an attached trailer | Physical damage/theft of the trailer asset; your business's liability exposure | Limits renter's out-of-pocket cost for specific covered damage events | | Not covered | Physical damage to the rented trailer; commercial rental activity | Renter's personal vehicle; damage from prohibited uses | Third-party liability; theft in non-qualifying circumstances | | Applies when | While the trailer is hitched and in motion | At all times the trailer is in your fleet, including when unhitched at a customer site | Only for covered damage events under the waiver terms | | Key Michigan note | Most personal policies exclude commercial rental activity [1][2] | Needed to fill the damage-to-the-trailer gap in standard GL [3] | Not insurance; adds a layer but does not replace commercial coverage [1][2] |

Coverage works only if every location follows the same pickup check.

Operational controls for contactless rentals, claims, and multi-location consistency

In Michigan, coverage holds up only when you can show who rented the trailer, what they agreed to, and what shape the trailer was in before and after the rental. Put simply: insurance is only as strong as your paperwork and proof.

That means every pickup needs to follow the same verification flow. No exceptions. No “we usually do it this way at this location.”

Before any trailer leaves the lot, run one repeatable checklist every time:

- Confirm the renter’s identity with a valid driver’s license

- Collect the tow vehicle details

- Verify that the renter’s Certificate of Insurance (COI) is current, including the expiration date, covered use, and minimum required limits

- Make sure the renter has accepted your rental terms

- Photograph the trailer from all four sides, plus the tires, hitch, and interior, with a timestamp

That COI step matters more than some operators think. If the policy limit is too low, you could still be left exposed when a claim goes past the renter’s coverage.[3]

Photos matter just as much. Take them at pickup, then do the same at return. Those images are often your first line of defense when someone later says, “That damage was already there.”

For contactless rentals, the process has to be enforced by the system, not left to memory. This is a core pillar of starting an automated trailer rental business. That’s where Lockii comes in. It blocks access until the renter uploads ID, submits a COI, and accepts the rental terms across every location. Michigan-specific terms and liability disclosures are built into the booking flow, so renters can’t claim they missed them.

Every action is logged with a timestamp, which gives you a clean audit trail for each rental. At return, photos are collected through the platform, and GPS tracking simplifies multi-location rentals by logging the trailer’s location during the rental. Those records can back up damage or theft claims. When every location follows the same process, claims are much easier to defend.

Conclusion: correct coverage plus controlled operations is the safest Michigan setup

Coverage handles the risk. Process proves compliance. In Michigan, defensible coverage depends on a standardized pickup process across every location.