Card Surcharges For Online Rental Bookings - Why You Should Never Do It

June 18, 2026 · 8 min read

Card Surcharges For Online Rental Bookings - Why You Should Never Do It

If you add a card surcharge at checkout, you can lose more in bookings than you save in fees.

I’d keep it simple: show the full rental price upfront, skip the last-step card fee, and bake processing costs into your base rate. That avoids checkout friction, cuts legal trouble, and protects trust in self-service booking flows.

Here’s the short version:

- Surcharges often appear too late in the booking flow

- Customers dislike surprise fees, and many leave when totals change

- Card rules and state laws are messy, especially for online bookings across states

- Debit and prepaid cards usually can’t be surcharged

- A small fee recovery can be wiped out by a small drop in conversion

- All-in pricing is the safer move for online rentals

A few numbers stand out:

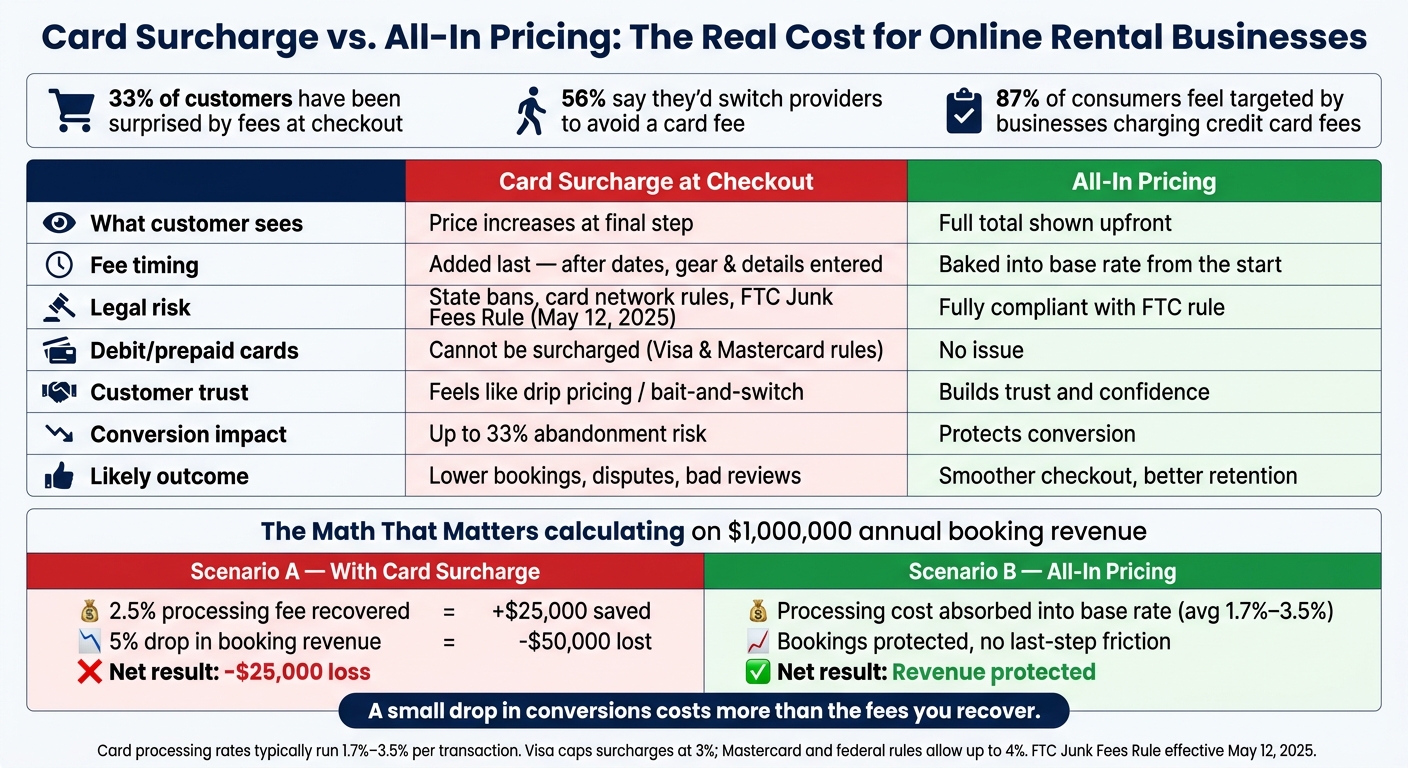

- 33% of customers say they’ve been surprised by fees at checkout

- 56% say they may pick another provider to avoid a card fee

- Card processing often runs 1.7% to 3.5%

- A 2.5% fee on $1,000,000 in bookings saves $25,000

- But a 5% drop in booking revenue can cost $50,000

| Option | What the customer sees | Main risk | Likely result | | --- | --- | --- | --- | | Card surcharge at checkout | Price goes up at the end | Abandonment, complaints, rule issues | Lower conversion | | All-in pricing | Full total shown early | Lower margin if priced wrong | Better trust and smoother checkout |

If I ran an online rental business, I would not add a card surcharge at the final payment step. I’d price cleanly from the start and make checkout feel simple.

What Card Surcharges Look Like in Online Rental Checkouts

What Counts as a Card Surcharge

A card surcharge is a 1.5% to 4% fee added only because the customer pays by credit card [1][3].

That’s the key point. This fee exists only because of the payment method. It’s meant to pass card processing costs to the renter.

That makes it different from charges like:

- a damage waiver (part of securing rentals without friction)

- a delivery fee

- other rental add-ons that apply no matter how the customer pays

There’s another rule many businesses miss: a surcharge cannot be applied to debit or prepaid cards, even if the customer clicks “credit” at checkout. Visa and Mastercard network rules bar that [1][2].

Where Surcharges Appear and Why Renters React Badly

In contactless rental models, the surcharge often shows up at the very end. The renter has already picked dates, chosen equipment, and filled in personal details. Then the final payment screen adds a new fee.

That’s where the friction starts.

The price the renter saw at the start no longer matches the final total. It feels like drip pricing, and it can come across like a bait-and-switch [6]. Even a small bump at that stage can throw people off. They were ready to pay, and now they have to stop and rethink the deal.

In the U.S., Visa caps surcharges at 3%, while Mastercard and federal rules generally allow up to 4% [1][3]. But the legal cap isn’t the same as customer comfort. A 2% or 3% fee added at the last step can still be enough to make a renter back out.

"Unexpected fees at checkout can increase cart abandonment online and create negative brand associations... If a customer is surprised by a surcharge, it can change their decision to buy from you." - Stripe [1]

Disclosure Does Not Equal Customer Acceptance

A lot of rental operators think disclosure solves the problem. It doesn’t.

Yes, card network rules say surcharges must be disclosed on the first page that mentions credit card brands, not just at the final confirmation screen [1][3]. That covers the rule side of things.

But customers don’t judge this only by the rulebook. They judge it by how it feels. And a surcharge can still feel unfair when it shows up after the renter has already spent time entering dates, gear choices, and contact details.

The data backs that up. A 2025 survey found that 87% of consumers felt they were being hit with extra fees by businesses charging credit card fees [8]. On top of that, 56% said they were likely to choose a different provider just to avoid the fee [7].

So disclosure may satisfy the network requirement. It does not remove the customer’s objection.

Why Card Surcharges Are Becoming a Legal and Commercial Risk

State Laws, Federal Scrutiny, and Card Network Rules

That frustration can turn into a legal issue fast. Card surcharges don't just hurt conversion. They can also create compliance problems.

The rules change from state to state. Some states ban surcharges. Others put a cap on them. And if you sell online, you may need to follow the rules tied to the customer's location, not just your own [3][8].

Card networks add another layer. They require proper notice, clear disclosure, and the right itemization on receipts [3][1]. On top of that, federal junk-fee enforcement is pushing businesses to show mandatory charges up front. So when a surcharge shows up only at the last payment step, it starts to look a lot like the kind of late-stage price increase regulators are already watching [6].

How Surprise Fees Lead to Disputes, Chargebacks, and Bad Reviews

The legal side matters, but the business hit shows up right away.

When a fee appears at the last step, customers often read it as a hidden charge. And they react fast. 32% of merchants that surcharge say customers cancel a purchase at least some of the time when the fee appears at checkout, while 68% of consumers now check most or all receipts because they're worried about hidden surcharges [7].

That kind of mistrust can snowball into disputes, bad reviews, and chargebacks. It's even worse when the surcharge isn't displayed the right way or when a debit card gets surcharged by mistake [2][4]. In contactless rentals, a checkout mistake doesn't just annoy the customer. It can kill the booking on the spot.

For rental operators, that means fewer bookings and weaker retention.

How Surcharges Cut Conversion and Cost More Than They Recover

Why Unexpected Fees Can Cut Bookings by Up to 33%

Even when a surcharge is allowed, it can still hurt bookings.

A fee added at the payment step gives people a reason to back out right before they finish. That’s the worst time to add friction. The customer is ready to pay, then suddenly sees an extra charge that wasn’t part of the price they had in mind. For rental operators, that last-step fee often feels less like pricing and more like a penalty.

And that friction isn’t just frustrating. It costs money.

The Math Rarely Works in Your Favor

In most cases, the numbers don’t pencil out. The fee is usually only 1.5% to 3.5% per transaction [1][8] - often just a few dollars. It doesn’t take much of a drop in bookings to erase those savings.

Here’s the simple math. On $1,000,000 in annual booking revenue, passing through a 2.5% processing fee saves $25,000. But if that surcharge leads to a 5% drop in booking revenue, the business gives up $50,000 in gross revenue. That leaves a net loss of $25,000 compared with absorbing the fee [4].

Transparent Pricing vs. Card Surcharge at Checkout: A Direct Comparison

All-in pricing protects conversion and trust. A card surcharge at checkout does the opposite.

The better move is simple: stop adding the fee separately and show the full price upfront.

What to Do Instead: Clear Pricing for Self-Service Rentals

Build Processing Costs Into Your Advertised Rental Rate

The simplest move is to build processing costs into the advertised rental rate.

Surcharges tend to backfire. They chip away at trust and can hurt conversion more than they make up for in fee recovery. Card processing is a normal cost of doing business, and in the U.S., merchants pay an average of 1.7% to 3.5% per transaction [3]. A smart next step is to review 3 to 6 months of processing statements, calculate your effective rate by dividing total fees by total volume, and roll that amount into your base price from day one [5].

Use Software That Shows the Full Booking Total From the Start

That approach only works if your booking flow shows the full total before the customer pays.

In contactless rentals, checkout needs to show the final price before the payment step. There’s no employee standing by to explain a last-minute fee in a 24/7 self-service setup. The checkout screen _is_ the sales process. Lockii is built for that flow: customers see the complete booking total before they reach payment, so the price doesn’t change at the last step.

The FTC's Junk Fees Rule, which took effect on May 12, 2025, requires covered businesses to display the total price, including every mandatory fee, the first time a consumer sees a listing [6]. For covered businesses, clean all-in pricing is now a legal rule, not just a smart move.

Conclusion: Drop the Surcharge, Protect Conversion, and Price Cleanly

Card surcharges bring legal risk and can hurt sales. State laws, card network rules, and customer expectations all point to the same thing: show the real price upfront [5][7].

The fix is straightforward: all-in pricing protects bookings, while hidden fees push people away. Set the price honestly, show the full total upfront, and use a booking system built to support that from the start.